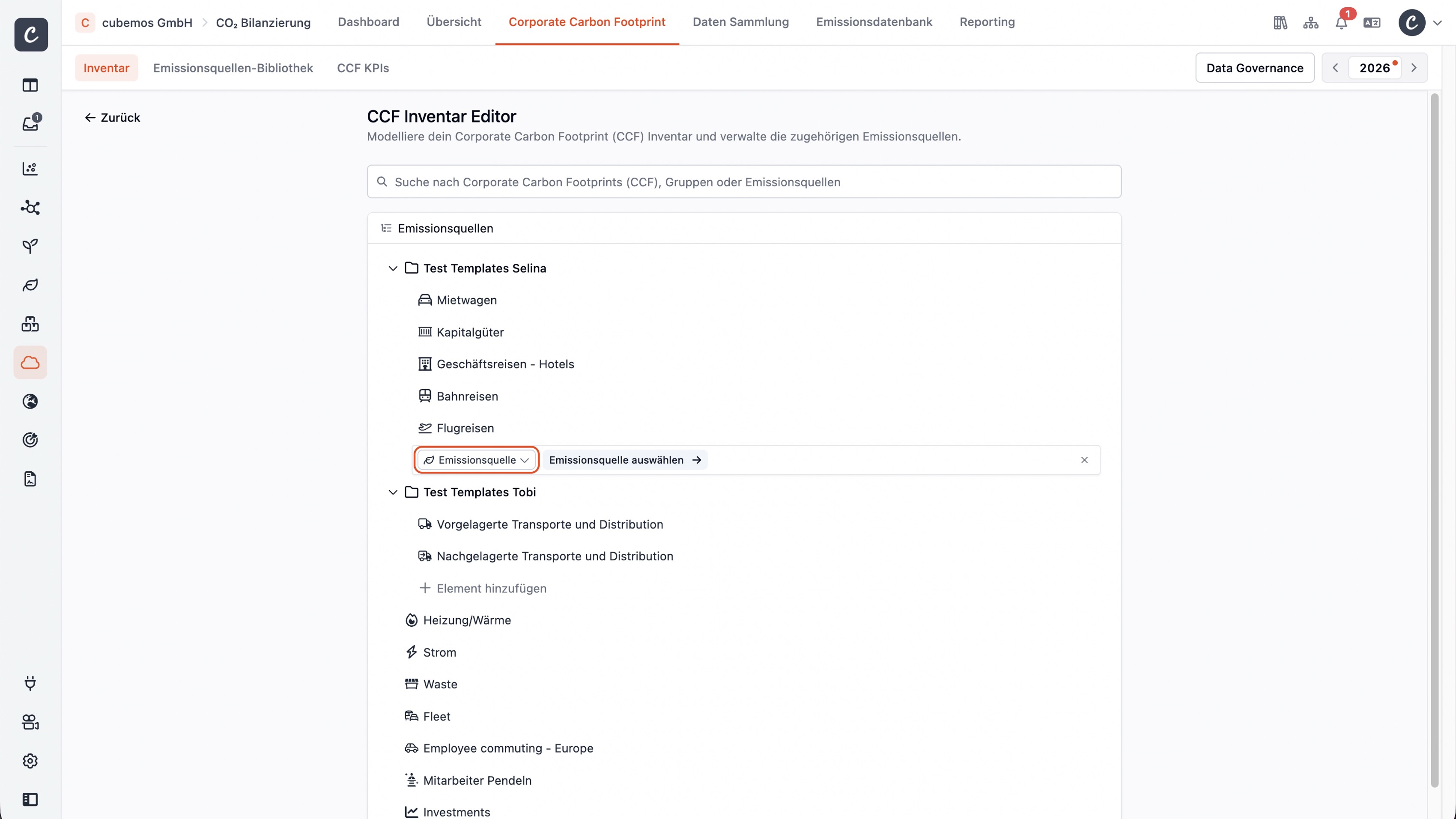

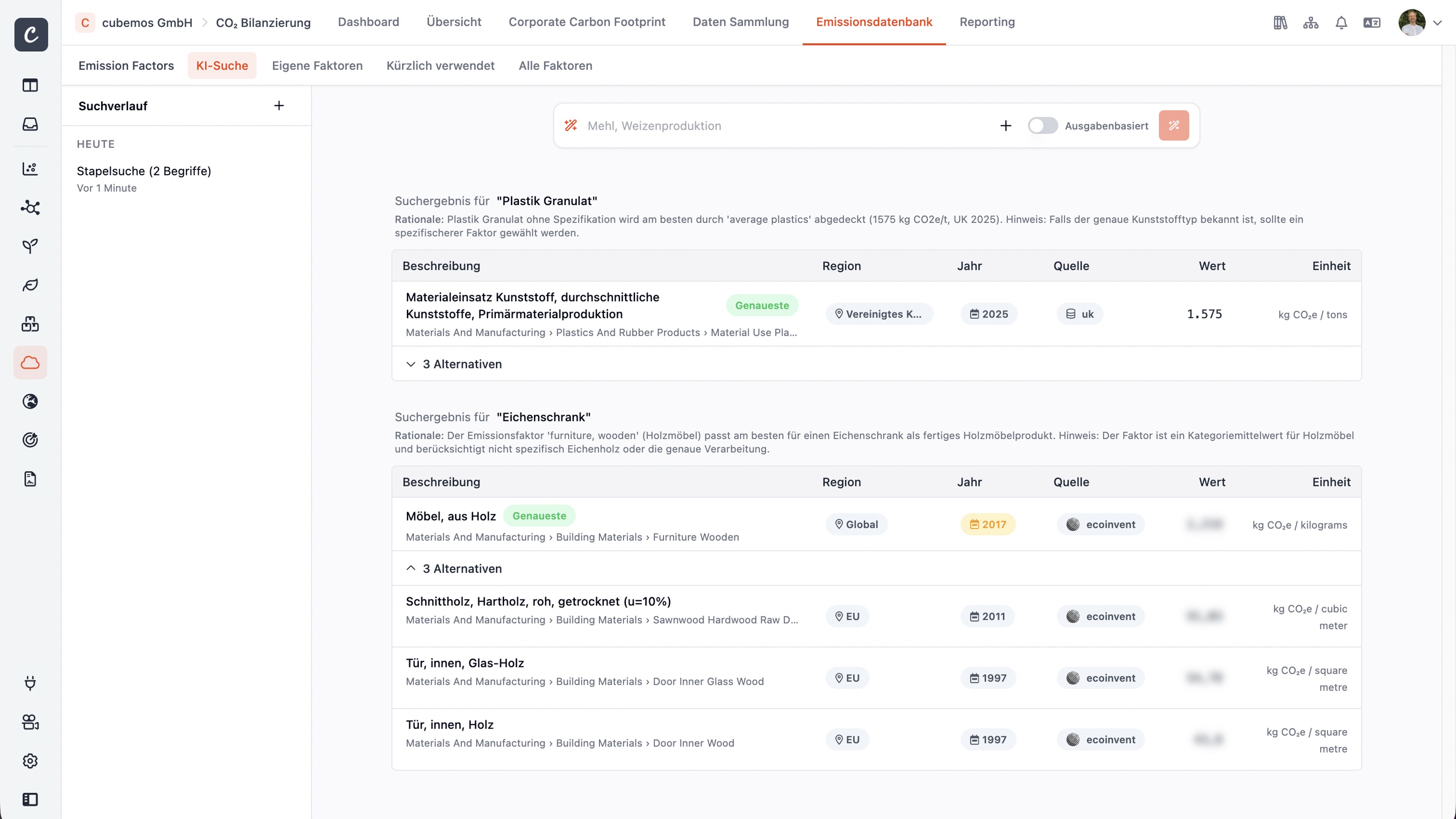

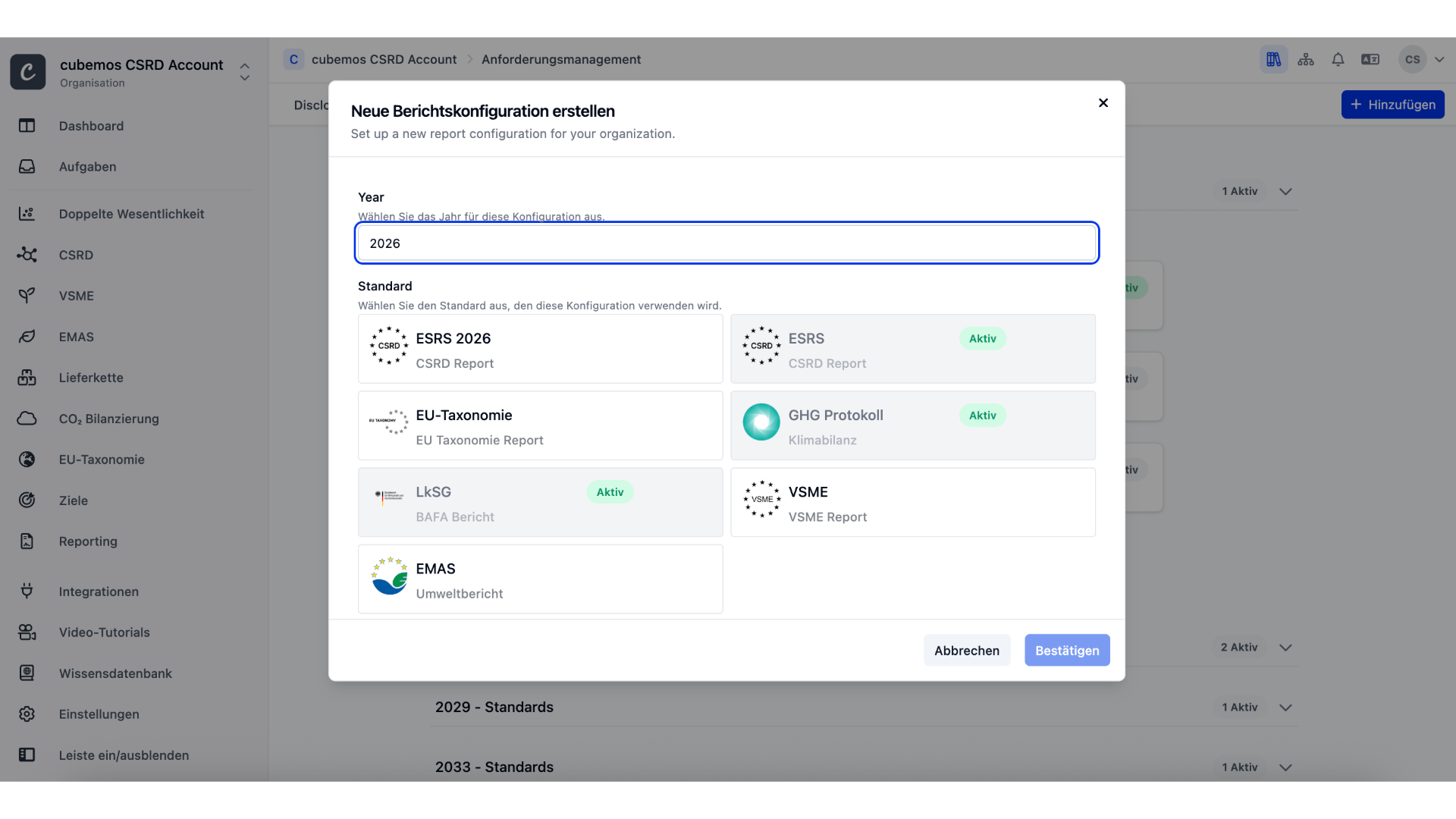

Select Scopes & Templates for Emission Sources

You can add scopes and emission sources to your greenhouse gas inventory with a single click. Tailored specifically to your company. What you don’t need is left out. New additions are ready to use immediately, with no setup required and no prior knowledge of the underlying calculations needed.

All emission factors are already stored for each source, in their current versions. All you have to do is enter what actually happens at your company: activities, quantities, or expenses. cubemos the rest for you—accurately, transparently, and based on sound methodology.

%20(1).avif)

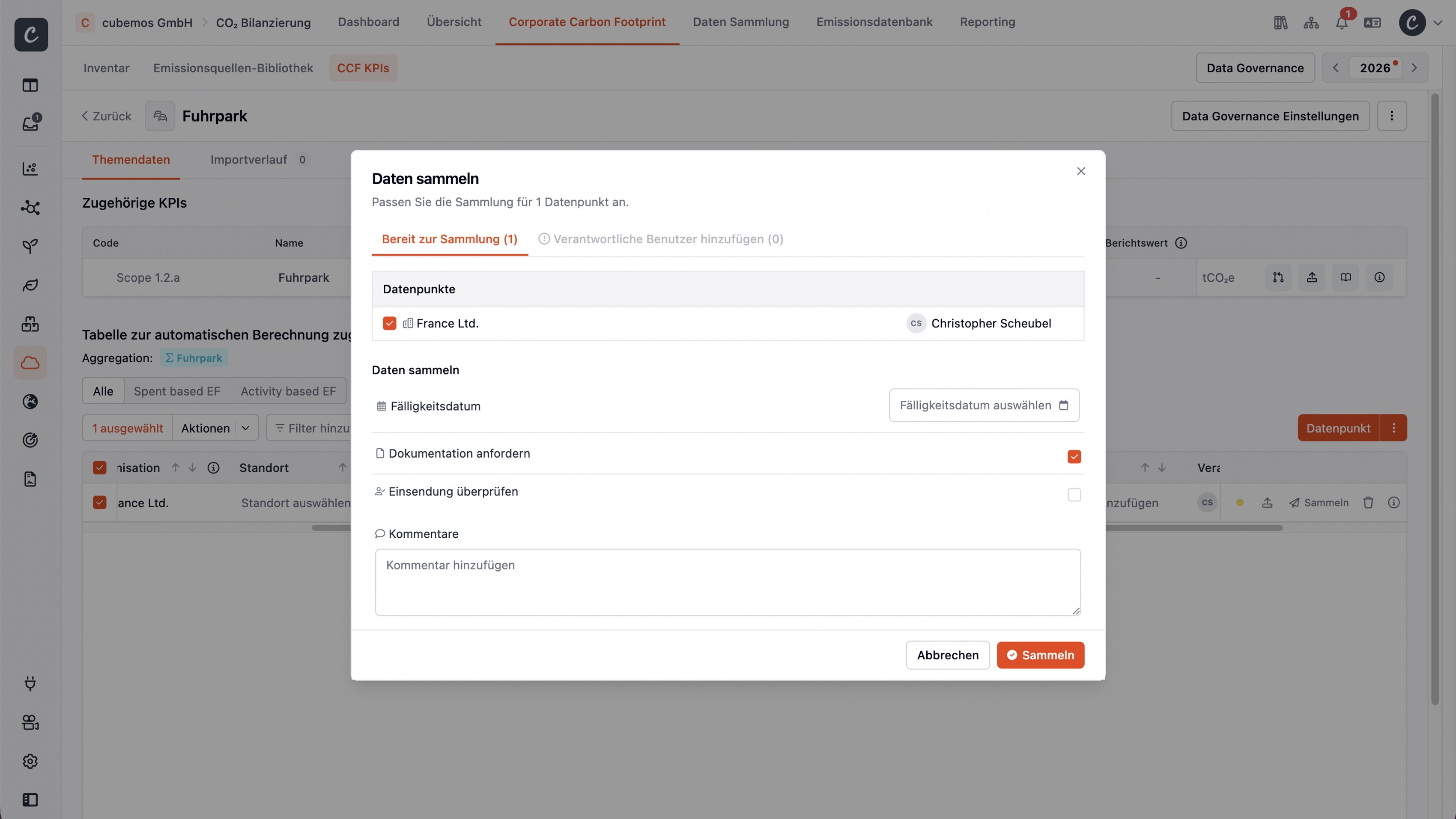

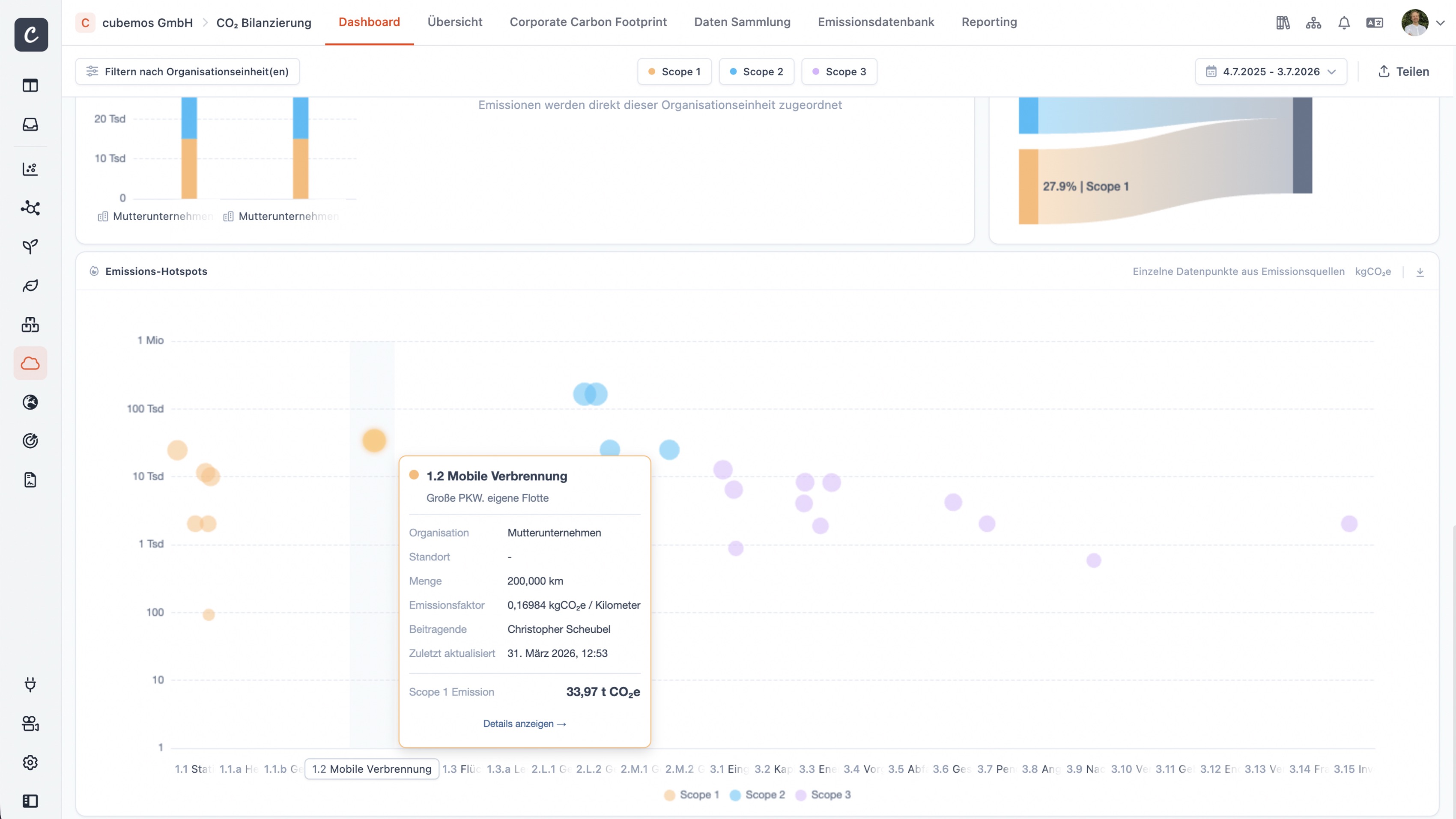

Collect Data Decentrally

Activity data directs you specifically to the right people—in the fleet department, in purchasing, and at the various locations—with a clear deadline and full context. It’s a task, not an endless email loop.

You can upload structured consumption and expense data as an Excel file, which is automatically mapped to the correct emission source. And when data is already stored in accounting, ERP, or fleet management systems, the REST API takes over: once connected, the data flows continuously into cubemos without any manual steps in between.

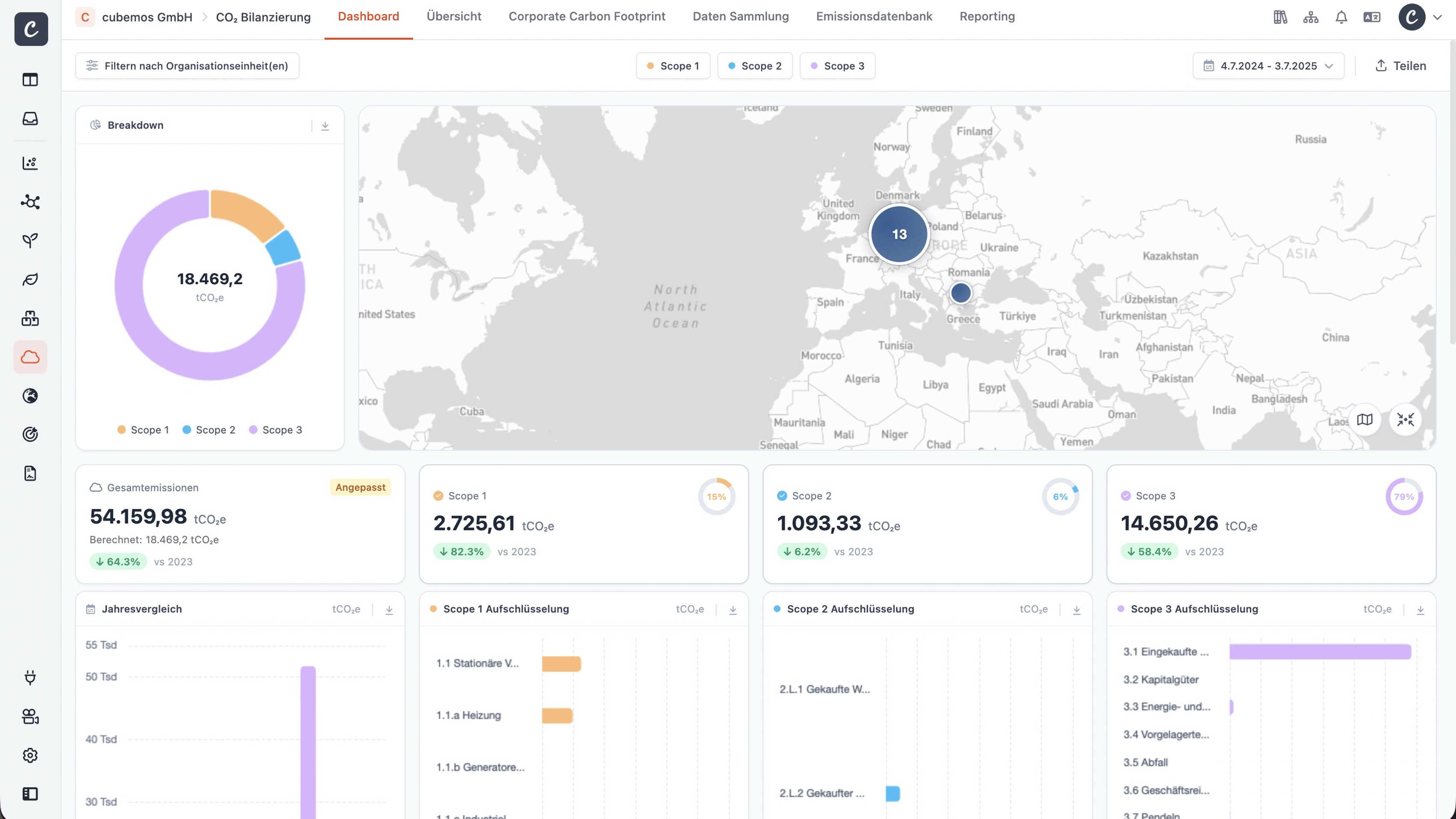

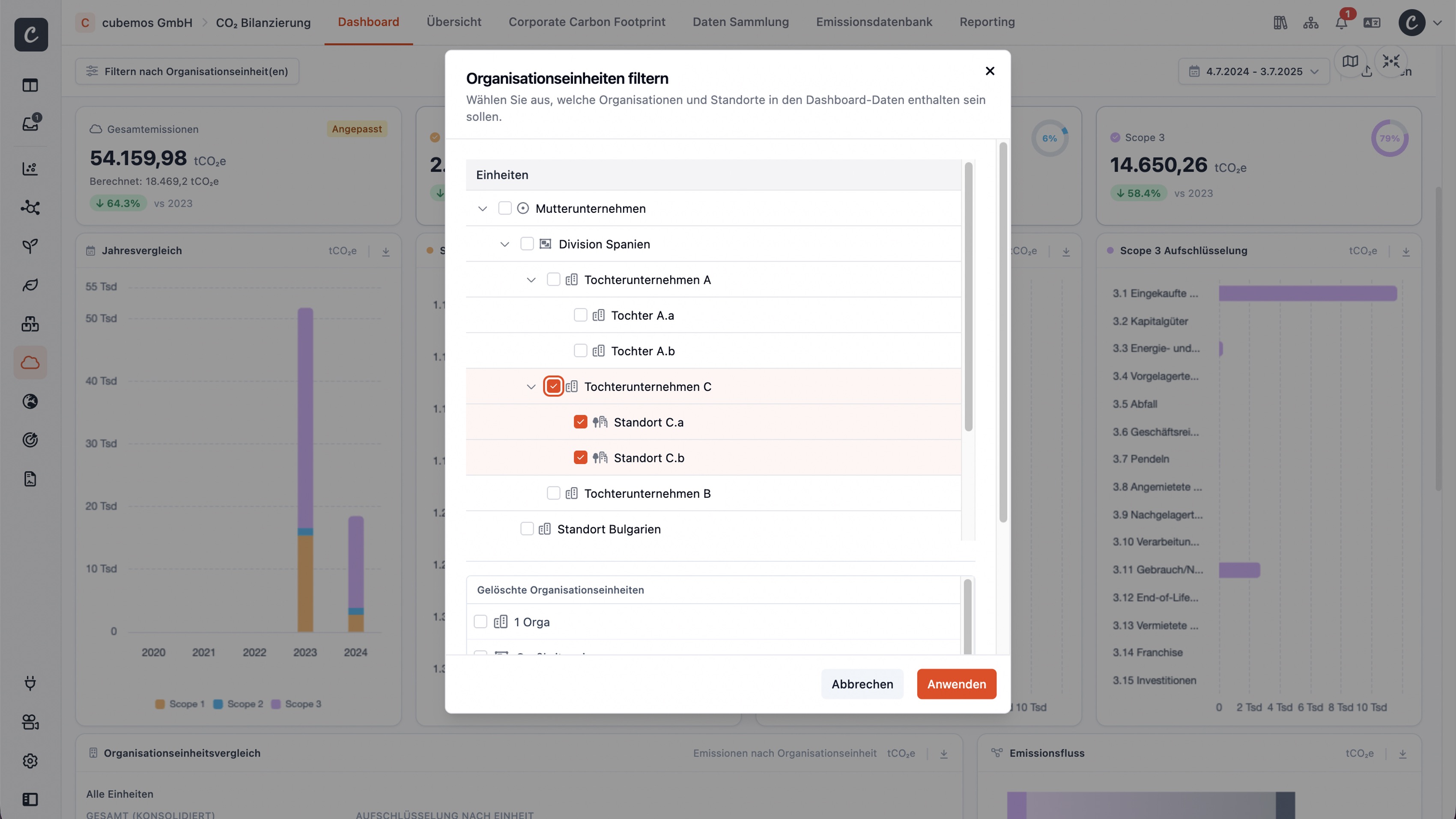

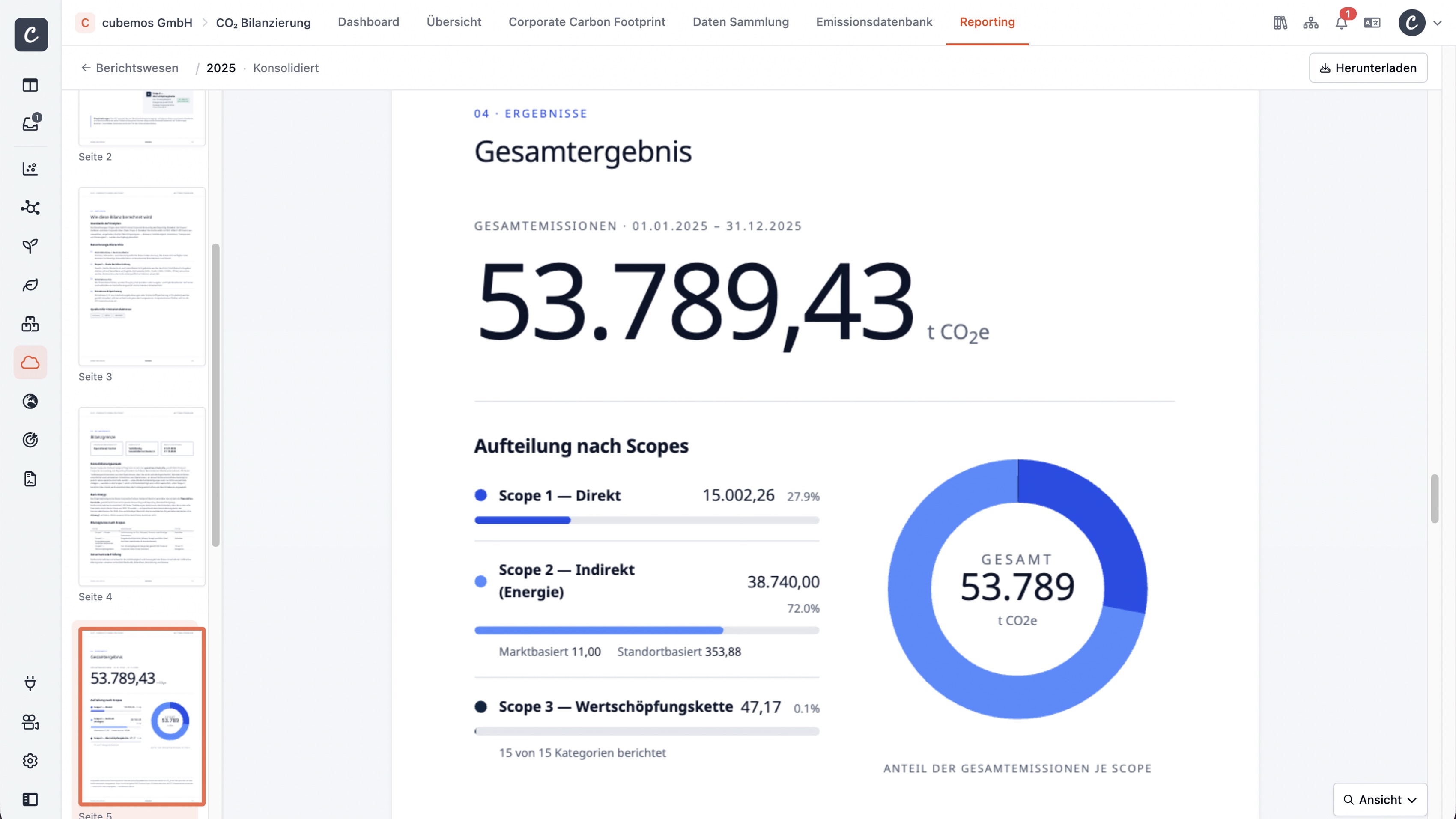

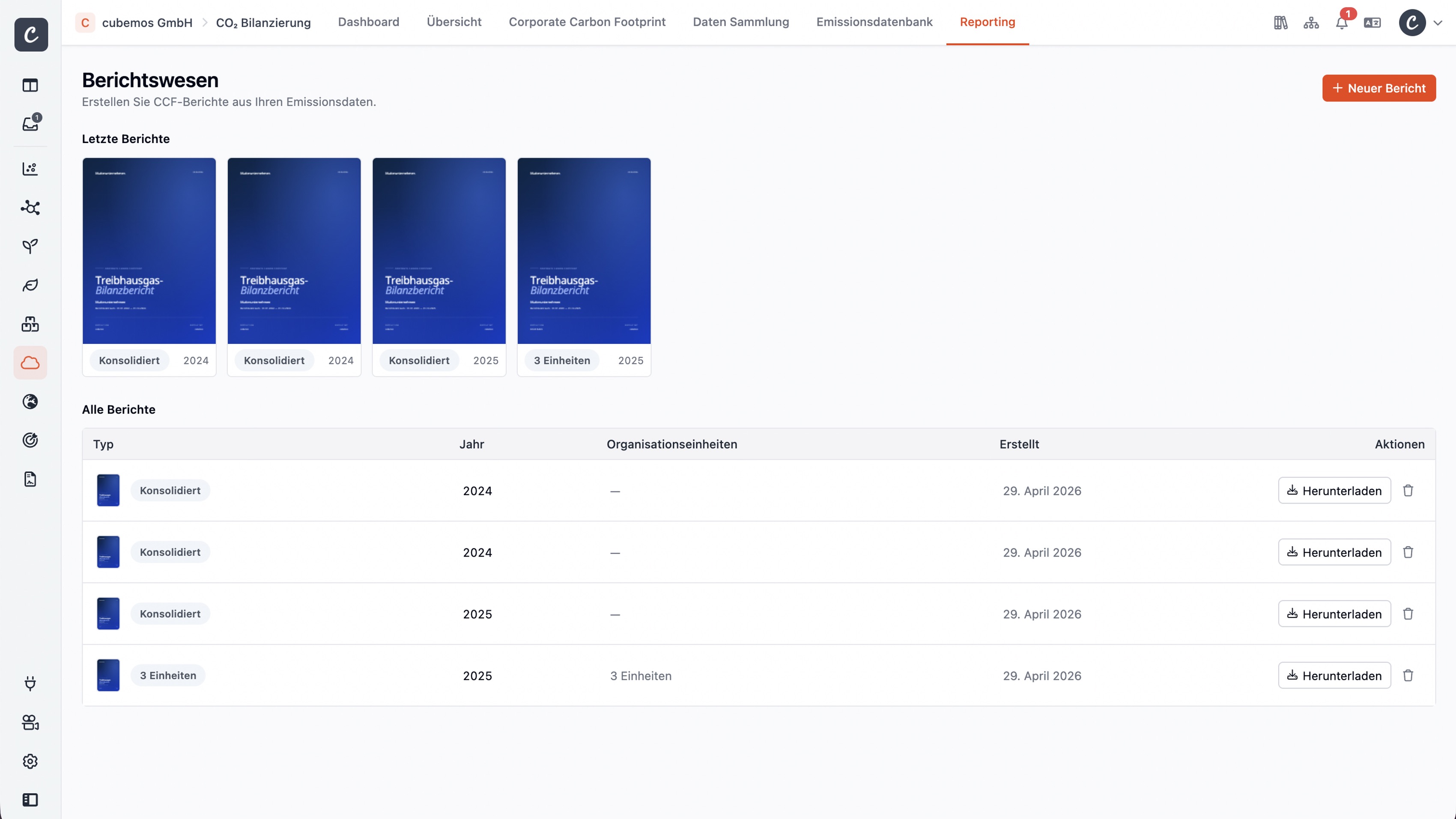

Conduct a benchmarking study within the company

Who’s where? Where are the highest emissions coming from, who’s performing better, and who needs support? cubemos the figures for all business units side by side—with a single click, without data exports, and without complicated Excel maneuvers. Breakdowns by scope, location, or division are visible in seconds.

Best of all: You share the analysis digitally with local management, directly from cubemos, without having to rely on slides or attachments. Financial statements become a tool for management. Numbers become decisions—right where they make a difference.

%20(1).png)

.avif)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.avif)